Client Primacy: Respecting Preference Within Fiduciary Care

by Nigel Valdez, CFF®, FRC®

Better Federal Retirement — Fiduciary Wealth Management for Federal Employees

When Fiduciary Care Meets Human Preference

As fiduciaries, our duty is clear: every recommendation must be in the best interest of our clients. But in real life, financial planning is not an algorithm—it’s human.

Many federal employees, for example, have a deep loyalty to the Thrift Savings Plan (TSP). It’s familiar, low-cost, and backed by the federal government—good reasons to like it.

Yet that comfort can also create a preference bias that leads to over-concentration, limited diversification, and missed opportunities.

Here’s where fiduciary care requires nuance. My role isn’t to impose my math on your preferences. It’s to ensure your preferences are informed—and that your ultimate decisions are made with full awareness of the tradeoffs.

The Duty of Client Primacy

Client primacy is the ethical principle that within the fiduciary relationship, the client’s informed preferences hold primacy—so long as those preferences are consistent with their goals, risk tolerance, and understanding of consequences.

In other words: I may know that a more sophisticated, risk-managed UMA could improve long-term outcomes. But if you understand the tradeoffs and still prefer to stay in your TSP—that’s your right. My duty is to educate, illustrate, and document. Not to override.

Client primacy is not passive acquiescence. It’s a process that ensures choices are made consciously, not reactively. It’s what distinguishes fiduciary care from salesmanship—dialogue instead of persuasion.

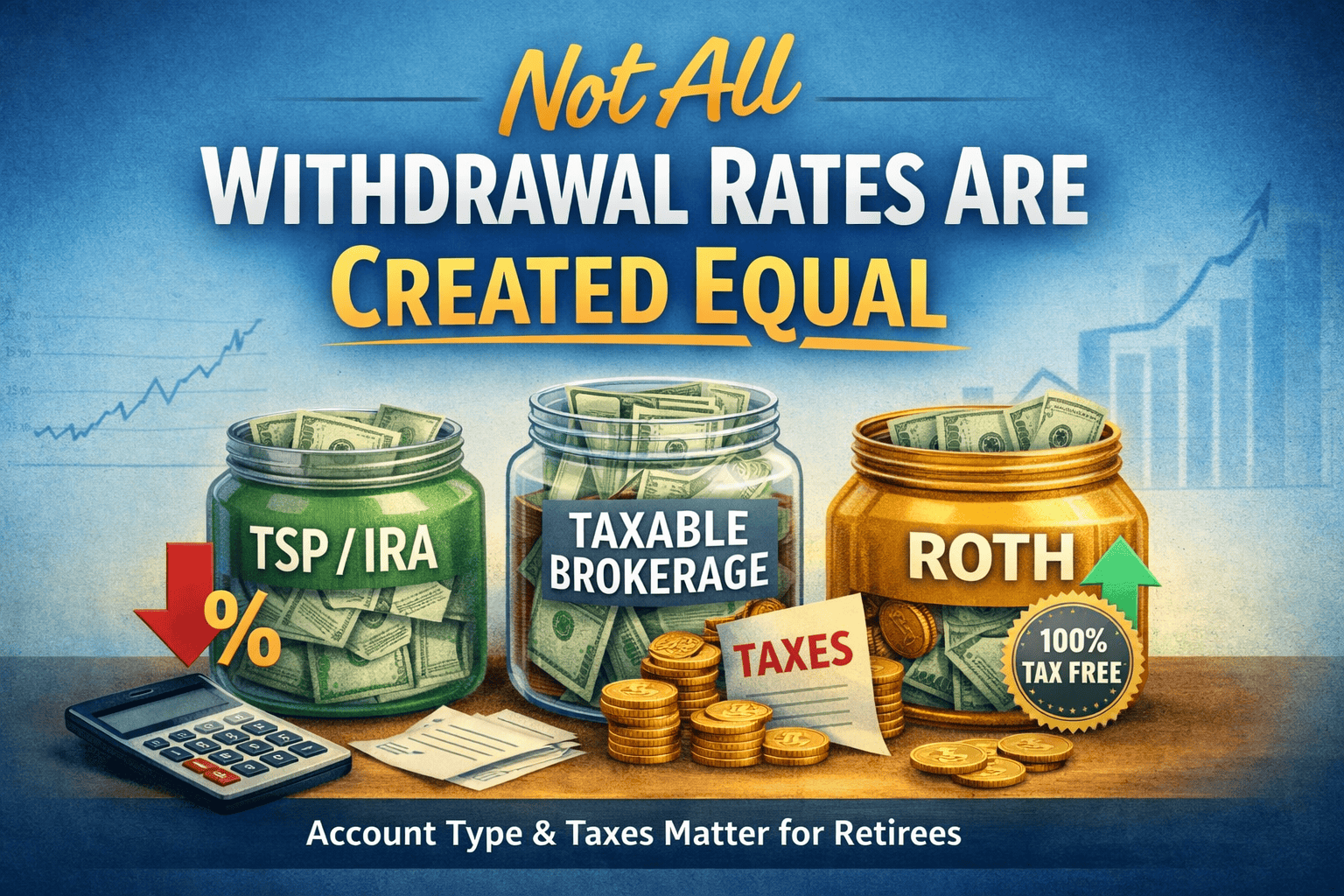

TSP Familiarity vs. Fiduciary Diversification

The TSP is exceptional in many ways: low fees, automatic payroll contributions, and straightforward fund choices. But as portfolios grow—particularly beyond $500,000—the TSP’s simplicity can become a limitation rather than a virtue. It generally lacks access to:

- Active risk-management tools such as hedged or long/short strategies

- Precious metals and alternative sleeves that add non-correlation

- Structured notes or buffered equity exposures

- Tax-sensitive income planning, charitable gifting, and location optimization

- Roth conversion & other tax management capability

- Values-aligned options (Faith-based, Environmental, etc…)

These aren’t “bells and whistles.” They’re instruments of institutional-grade diversification. Still, if your preference is to keep a portion in TSP—because it represents security, identity, or trust—then honoring that preference is part of fiduciary care. Our task is to balance that psychological value with the data-driven pursuit of better long-term outcomes.

Respect, Dialogue, and Documentation

At Better Federal Retirement, fiduciary advice isn’t just about math—it’s about meaning. We document every recommendation, but also every preference. We test assumptions, but also respect beliefs. We blend analytics and empathy, because the right plan is the one you can understand, believe in, and stick with. The right plan, is yours.

Better Planning. Better Investing. Better Retirement.

If you’ve built significant wealth inside the TSP and wonder whether keeping it is still the best fit—or if it’s simply the most familiar—let’s explore that together.

Educational information only. Not investment, tax, or legal advice. Advisory services offered by Better Federal Retirement, a fiduciary and fee-only firm. All investing involves risk, including possible loss of principal.

Leave a Comment