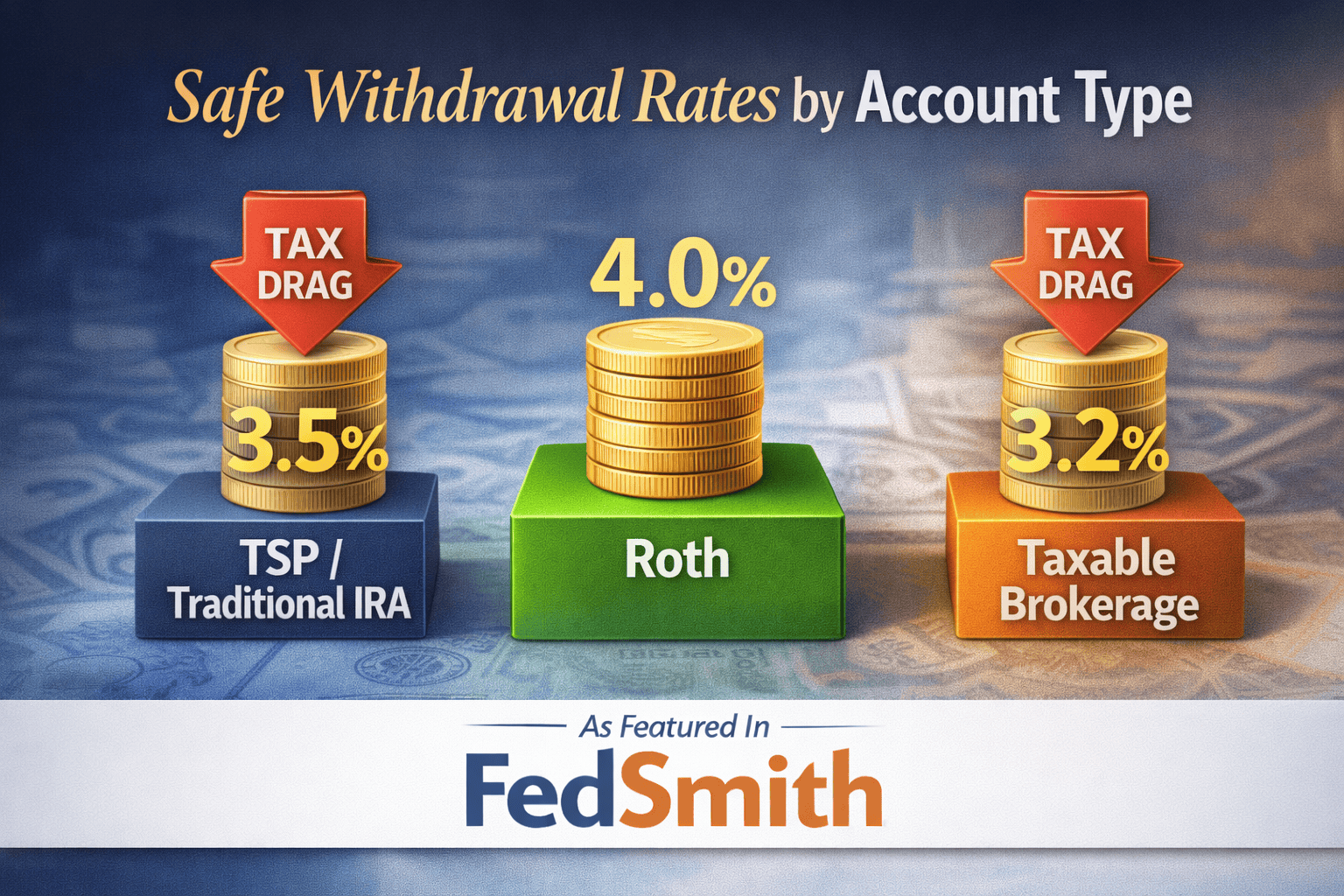

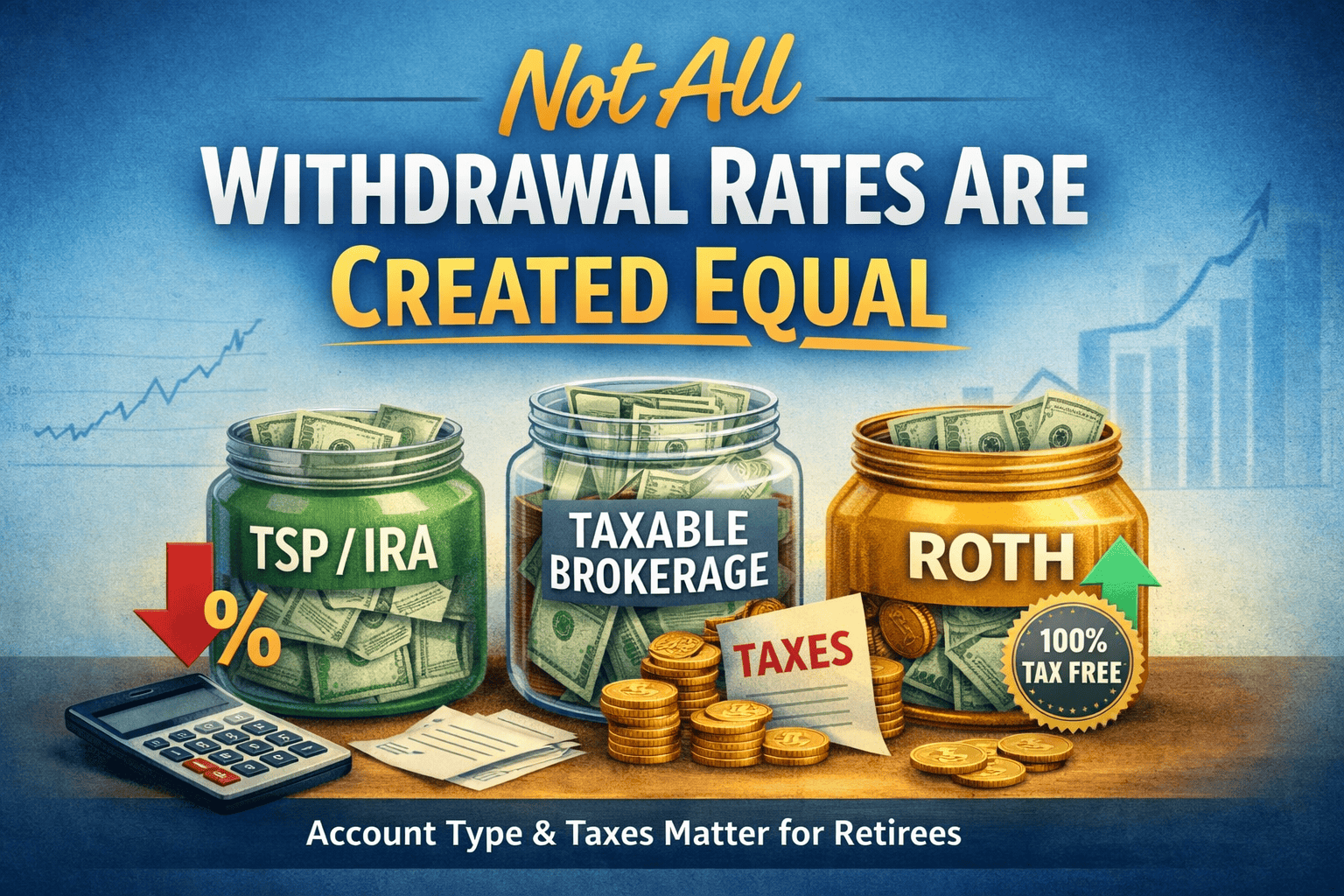

The “4% rule” is one of the most widely cited guidelines in retirement planning—but it’s often misunderstood, especially by federal employees.

In this FedSmith article, I explain why safe withdrawal rates aren’t universal—and how the type of account you’re spending from can significantly impact how much you can safely withdraw.

Because taxes affect each account differently, two retirees with identical portfolios may have very different sustainable income levels. Understanding that difference is key to building a retirement income strategy that actually works over time.

Leave a Comment