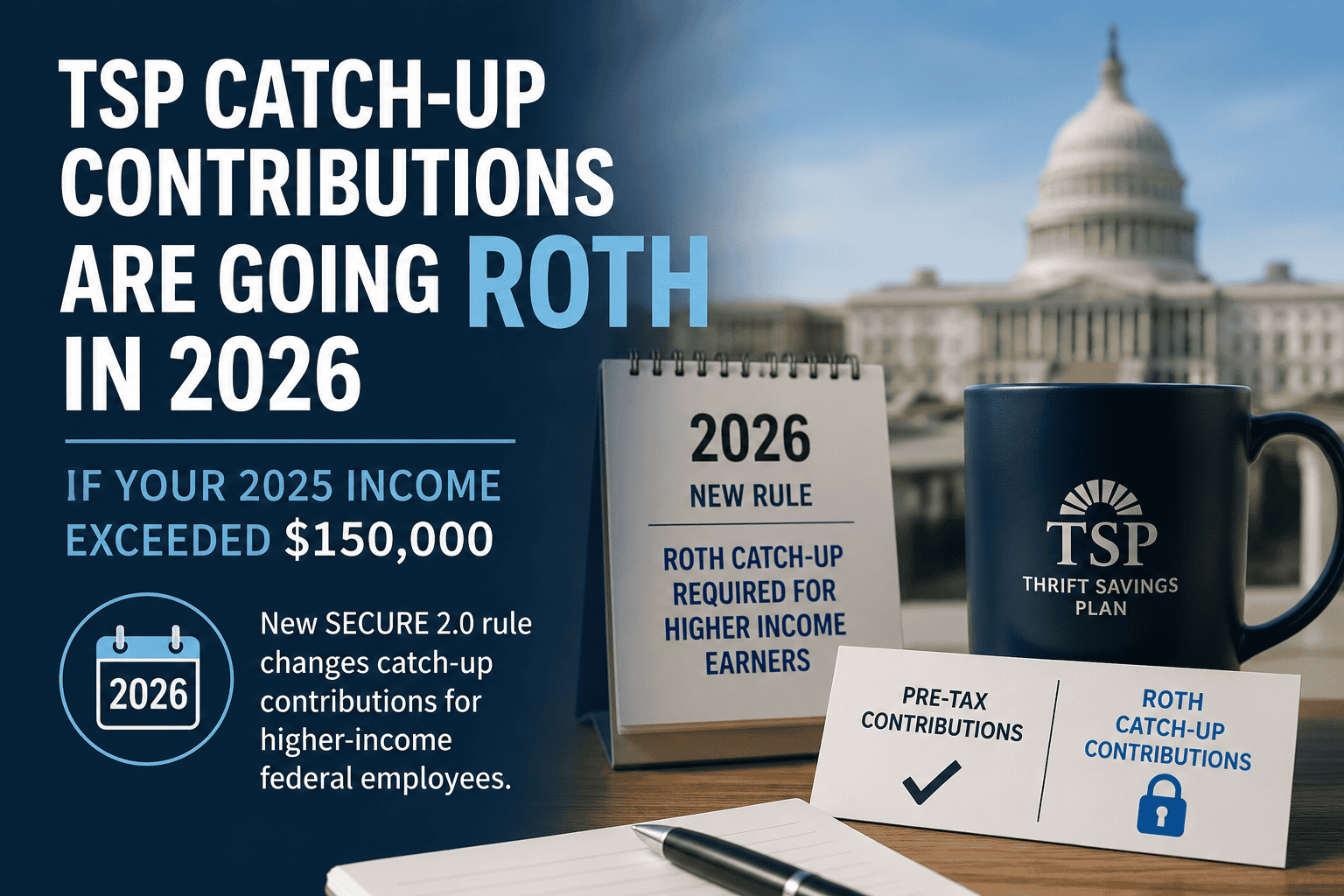

TSP Catch-Up Contributions Forced To Go Roth in 2026 — If Your 2025 Income Exceeded $150,000

You are affected if…

- ✅ You are age 50 or older

- ✅ Your 2025 FICA wages — Social Security wages on your W-2 — exceeded $150,000 (if you made $149,999 you aren’t affected)

- ✅ You plan to make catch-up contributions to the TSP in 2026

All three must apply. If any one of them doesn’t, this rule doesn’t affect you, yet.

What’s Actually Changing

Under SECURE 2.0, employees who meet the income threshold above will be required to direct their catch-up contributions into the Roth side of the TSP — not the traditional pre-tax side.

A few important clarifications:

- Only the catch-up layer is affected. Your regular TSP contributions, up to the standard annual $24,500 limit, can still go in pre-tax Traditional.

- It’s a hard cliff, not a phase-out. One dollar over the income threshold means all of your catch-up contributions must be Roth.

- It’s based on prior-year FICA wages — not AGI, not taxable income. TSP contributions and FEHB deductions don’t reduce the number being tested.

The same rule applies to 401(k), 403(b), and governmental 457(b) plans — but for federal employees, the TSP is what matters.

Two Examples

Maria, age 57 — GS-15, Step 8

Maria’s 2025 FICA wages come in at $150,001. In 2026, she plans to contribute the standard TSP limit plus the standard catch-up contribution.

Under the new rule, her $24,500 regular contributions can still be traditional pre-tax. But the $8,000 catch-up contribution must go into her Roth TSP. That is money she will not get to deduct — which, depending on her marginal rate, could mean more federal taxes for the year.

David, age 60 — Senior Executive

David is between ages 60 and 63, which means SECURE 2.0 gives him access to a larger $11,250 “super catch-up” contribution. His income well exceeds the threshold.

All of that super catch-up must go Roth. The trade-off is real: more taxable income now, but potentially meaningful tax-free assets in retirement. Whether that trade makes sense depends on where David expects to land in retirement and how his Roth conversion strategy is already structured.

Why This Gets Complicated

Roth vs. pre-tax is not just a TSP question. The decision ripples into:

- Current-year taxes — higher income means higher rates and potentially different bracket exposure (you may get a bigger tax bill than expected)

- Medicare IRMAA — income two years prior determines Medicare Part B and Part D premiums; a spike now can show up in your premiums later (so be sure to file your SSA-44 when you retire!)

- Roth conversion planning — if mandatory Roth catch-ups are pushing income up, the math on additional conversions changes (of course, most Roth conversions happen post-separation)

For some federal employees, forced Roth catch-ups will actually fit neatly into a plan that was already leaning that direction.

For others — particularly those using pre-tax contributions to actively manage their tax picture before retirement — this adds complexity and challenge.

This Is the Kind of Planning We Do

If you are within ten years of retirement and you are unsure how this change fits into your overall tax and income plan, this is exactly the kind of question Better Federal Retirement was built to answer.

Leave a Comment